Luxembourg Financial Regulatory News:

On April 10, 2026, the Commission de Surveillance du Secteur Financier (CSSF) announced the launch of the “LMT activation” module within its eDesk portal. This initiative follows the transposition of Directive (EU) 2024/927 into Luxembourg law via the Law of 3 March 2026. The new module mandates that Luxembourg-domiciled UCITS and authorised Alternative Investment Fund Managers (AIFMs) electronically notify the CSSF regarding the activation and deactivation of specific liquidity management tools.

Key milestones include the prior launch of an “LMT selection” module on March 23, 2026, and a hard deadline of April 16, 2026, for both the initial selection disclosures and the commencement of the new activation notification requirements. This regulatory framework aims to enhance transparency and facilitate the mandatory sharing of liquidity data with the European Securities and Markets Authority (ESMA) and the European Systemic Risk Board (ESRB).

Regulatory Framework and Legal Basis under CSSF Communication to the investment fund industry regarding the “LMT activation”

The transition to electronic LMT reporting is driven by recent legislative updates intended to harmonize liquidity management across the European Union.

- Primary Legislation: The Law of 3 March 2026 transposes Directive (EU) 2024/927 of the European Parliament and of the Council (13 March 2024).

- Sectoral Impact: This law amends two foundational statutes in Luxembourg finance:

- The 2010 Law: Relating to undertakings for collective investment (UCIs).

- The 2013 Law: Relating to Alternative Investment Fund Managers (AIFMs).

- Supervisory Objectives: Information collected via the eDesk procedure is utilized by the CSSF to notify relevant competent authorities, ESMA, and, where applicable, the ESRB.

The eDesk LMT Procedure under CSSF Communication to the investment fund industry regarding the “LMT activation”

The CSSF has established a two-pronged electronic procedure via the eDesk platform to manage LMT disclosures.

1. The “LMT Selection” Module under CSSF Communication to the investment fund industry regarding the “LMT activation”

Launched on March 23, 2026, this module requires fund managers to:

- Communicate their selection of available LMTs.

- Submit detailed policies and procedures governing the activation and deactivation of these tools.

- Deadline: Submissions must be completed by April 16, 2026.

2. The “LMT Activation” Module under CSSF Communication to the investment fund industry regarding the “LMT activation”

Launched on April 10, 2026, this module is the primary vehicle for real-time notifications of tool usage.

- Effective Date: Mandatory use begins April 16, 2026.

- Purpose: Notification of the activation or deactivation of liquidity measures.

Scope of Application under CSSF Communication to the investment fund industry regarding the “LMT activation”

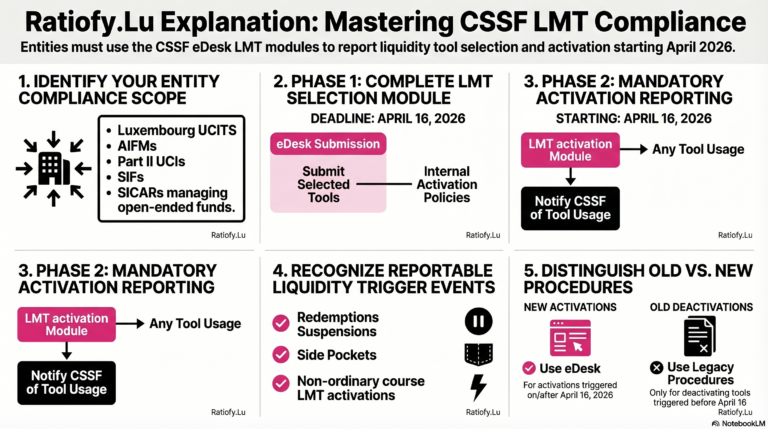

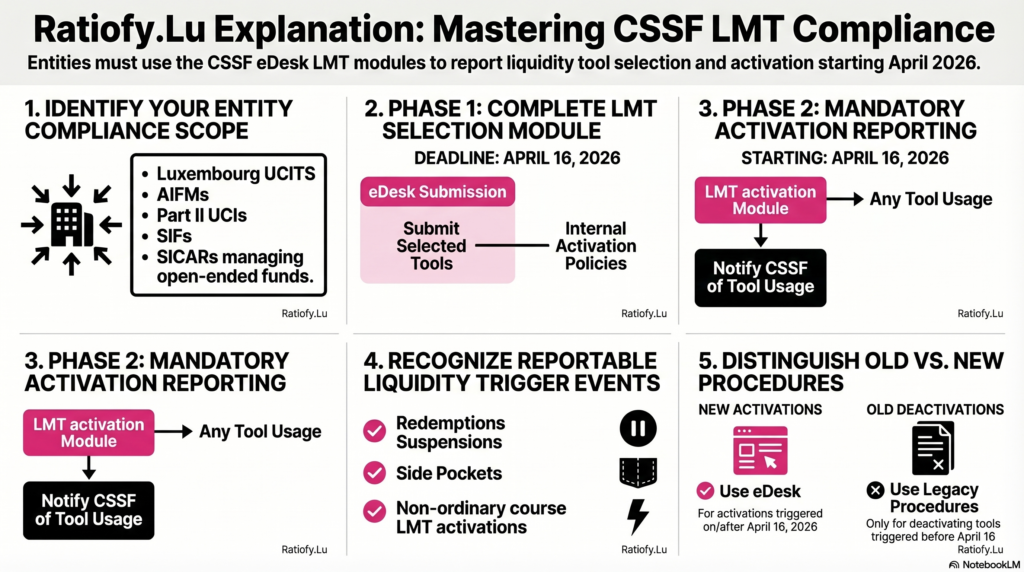

The reporting requirements apply to a broad range of investment vehicles and managers domiciled or authorized in Luxembourg.

| Entity Type | Reporting Requirement |

| UCITS / Management Companies | Must report LMT selection and activation/deactivation for Luxembourg-domiciled UCITS. |

| Authorised AIFMs | Must report for all managed open-ended Alternative Investment Funds (AIFs). |

| Part II UCIs | Must notify regarding suspensions and side pockets if not managed by a Lux-authorised AIFM. |

| SIFs and SICARs | Specialized Investment Funds and Risk Capital companies must report suspensions and side pockets if not managed by a Lux-authorised AIFM. |

Notification Requirements and Thresholds under CSSF Communication to the investment fund industry regarding the “LMT activation”

The CSSF distinguishes between different types of liquidity actions that require notification through the “LMT activation” module.

Mandatory Notifications under CSSF Communication to the investment fund industry regarding the “LMT activation”

As of April 16, 2026, entities must notify the CSSF of the following:

- Suspensions: Any suspension of subscriptions, repurchases, or redemptions.

- Side Pockets: The creation or closing of side pockets. Note: For side pockets, the CSSF must be notified within a reasonable timeframe before the activation or deactivation.

- Non-Ordinary Course Actions: The activation of any LMT referred to in Annex III (2010 Law) or Annex V (2013 Law), specifically when applied “in a manner that is not in the ordinary course of business” as defined in the fund’s rules or instruments of incorporation.

Transition Rules and Exceptions under CSSF Communication to the investment fund industry regarding the “LMT activation”

The CSSF has implemented specific guidelines for the transition to the new system:

- Pre-existing Activations: If an LMT was activated before April 16, 2026, its subsequent deactivation must not be reported through the eDesk “LMT activation” module. Instead, managers must follow the “usual CSSF procedure” for these legacy cases.

- Module Exclusivity: The “LMT activation” module is strictly reserved for notifications occurring on or after the April 16 effective date.

Key Compliance Dates under CSSF Communication to the investment fund industry regarding the “LMT activation”

| Date | Milestone |

| 18 March 2026 | Initial CSSF Communiqué announcing the eDesk procedure. |

| 23 March 2026 | Launch of the “LMT selection” module. |

| 10 April 2026 | Launch of the “LMT activation” module. |

| 16 April 2026 | Deadline for “LMT selection” submissions. |

| 16 April 2026 | Mandatory start date for “LMT activation” notifications. |

This news related to under CSSF Communication to the investment fund industry regarding the “LMT activation” can be considered beneficial under CSSF-Circulars, EU Regulations, Explanation, IFMs (AIFMs, ManCos) News, Investment Firms News, Undertakings for collective investment (UCIs).

At https://Ratiofy.Lu/, we defend your hard-earned money with our free daily news platform and expert-vetted templates. Need more help? Request access to our hands-on expert Advisory, Training and Coaching Services (very limited availability) related to CSSF Circulars and EU Regulations.

The pre-filled example templates for many CSSF Circulars should be available at https://ratiofy.lu/templates/ from the summer of 2026.

Takeaway 1: The End of Manual Notifications – The eDesk Era is Here under CSSF Communication to the investment fund industry regarding the “LMT activation”

The CSSF has sounded the death knell for manual notifications for Luxembourg-domiciled UCITS and Luxembourg-authorised Alternative Investment Fund Managers (AIFMs) managing open-ended AIFs. Under the Law of 3 March 2026, electronic communication is now the non-negotiable standard.

This is more than a simple platform update; it is a strategic pivot toward “RegTech” as an enforcement mechanism. By forcing notifications into standardized digital modules, the CSSF is eliminating the ambiguity of legacy reporting. Transparency is no longer a conversation—it is a data stream. For the strategist, this means your compliance department’s speed is now tethered to your digital proficiency.

“Luxembourg-domiciled UCITS… and Luxembourg-authorised AIFMs managing open-ended AIFs are required to electronically communicate to the CSSF the LMT-related information.”

Takeaway 2: Beyond the Ordinary – Defining What Triggers a Report under CSSF Communication to the investment fund industry regarding the “LMT activation”

The CSSF is not interested in your daily operational rhythm. The eDesk module is reserved for high-impact events: suspensions of redemptions/subscriptions, the creation of side pockets, and the activation of specific LMTs when used “in a manner that is not in the ordinary course of business.” Crucially, for side pockets, the regulator now mandates notification within a “reasonable timeframe before” activation or deactivation—a “pre-notification” requirement that necessitates tight internal coordination.

The focus on “non-ordinary” activations is a clear signal. The regulator is building a dashboard for market stress, filtering out the “noise” of routine adjustments to focus exclusively on deviations from a fund’s instruments of incorporation. This ensures that when a fund manager steps outside their standard playbook, the CSSF has immediate visibility.

“any LMT referred to in Annex III, points 2 to 8 of the 2010 Law or Annex V, points 2 to 8 of the 2013 Law, in a manner that is not in the ordinary course of business, as envisaged in the UCITS or AIF rules or instruments of incorporation.”

Takeaway 3: The Regulatory Chain Reaction – From Luxembourg to ESMA under CSSF Communication to the investment fund industry regarding the “LMT activation”

Perhaps the most impactful takeaway for the C-suite is the realization that a liquidity crisis is no longer a private conversation with the CSSF. A single entry in the Luxembourg eDesk portal triggers an immediate regulatory chain reaction. This data is automatically used to notify the European Securities and Markets Authority (ESMA) and, where applicable, the European Systemic Risk Board (ESRB).

This interconnectedness elevates a local liquidity event into a European systemic risk data point. Managers must recognize that their eDesk submissions will likely form the basis of future ESMA thematic reviews. You aren’t just filing a report; you are contributing to a pan-European surveillance map that invites broader scrutiny from top-tier supervisors.

Takeaway 4: The April 16th “Grandfathering” Trap under CSSF Communication to the investment fund industry regarding the “LMT activation”

The industry must navigate a counter-intuitive “grandfathering” trap. The “LMT activation” module becomes mandatory on April 16, 2026. However, its use is strictly tied to the date of the activation event.

If a tool—such as a redemption suspension—was activated on April 15, 2026, its subsequent deactivation must follow the old manual procedure. If it is activated on April 17, you must use eDesk. This creates a messy “two-track” reality for firms managing legacy issues. Furthermore, you cannot activate via eDesk if you failed to comply with the “LMT Selection” module requirements (launched March 23, 2026), which required the upload of detailed policies by the same April 16 deadline. The “trap” lies in assuming the new portal simply replaces the old; in reality, firms must maintain dual workflows for legacy activations until they are fully wound down.

Takeaway 5: Expanded Scope—It’s Not Just for UCITS under CSSF Communication to the investment fund industry regarding the “LMT activation”

The CSSF has ensured there are no “digital blind spots” in the Luxembourg fund industry. The notification mandate extends to Part II UCIs, Specialised Investment Funds (SIFs), and Investment Companies in Risk Capital (SICARs) that do not qualify as AIFs or aren’t managed by a Luxembourg-authorised AIFM.

These entities are now under the same digital umbrella for critical actions like side pockets or redemption suspensions. This broad-spectrum regulatory tightening ensures that even niche investment vehicles are integrated into the CSSF’s centralized scrutiny framework. No corner of the market is exempt from this digital evolution.

Conclusion: The Future of Liquid Markets under CSSF Communication to the investment fund industry regarding the “LMT activation”

The rollout of these eDesk modules marks a new frontier where regulatory response time is measured in clicks rather than weeks. By digitizing the lifecycle of Liquidity Management Tools—from selection to activation—the CSSF is preparing for a future where data precision drives systemic stability. As the AIFMD II era begins in earnest, the question for fund managers is no longer just about having enough liquidity—it’s about having the digital agility to report it. Are your internal policies robust enough to survive the scrutiny of a real-time ESMA data feed, or are you still relying on the “email-and-hope” strategies of the past?