Luxembourg Financial Regulatory News:

CSSF Circulars:

Let’s understand the new rules and instructions regarding Liquidity Management Tools (LMTs). These guidelines were created by the European Securities and Markets Authority (ESMA) and are being applied in Luxembourg by the Commission de Surveillance du Secteur Financier (CSSF) through Circular 26/910.

Summary

The primary goal of these guidelines is to ensure that investment fund managers have the right tools to handle cash flow challenges (liquidity risks) and to protect the stability of the financial system.

The most critical points to understand are:

- Manager Responsibility: Fund managers are primarily responsible for choosing, setting up, and using these tools.

- Suitability: Tools must be chosen based on the specific nature of the fund, such as its investors, what it invests in, and how often investors can buy or sell.

- Fairness: The tools must protect the interests of all investors and prevent “dilution,” which is when the costs of trading by some investors reduce the value of the fund for those who stay.

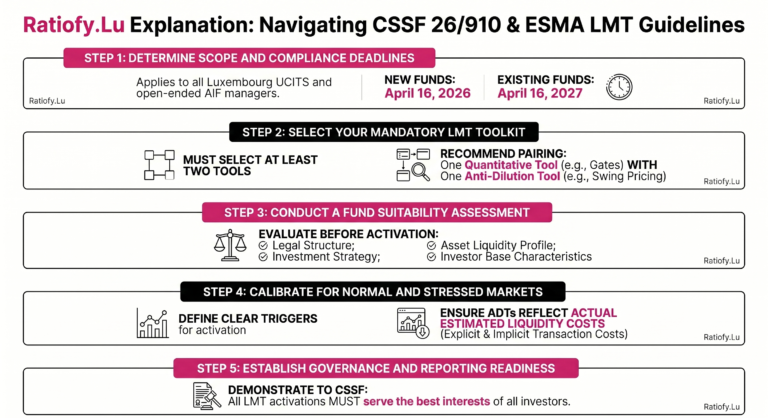

- Timeline: The rules begin to apply on April 16, 2026. Funds that already exist before that date have an extra year to comply, until April 16, 2027.

1. Scope and Affected Entities under Circular CSSF 26/910: ESMA Guidelines on Liquidity Management Tools (LMTs) of UCITS and open-ended AIFs

The circular applies to various investment fund managers (IFMs) in Luxembourg. The following table identifies who must follow these rules and who is recommended to consider them.

| Category | Specific Entities |

| Required to Comply | Management companies (Chapter 15 and Article 125-2); Luxembourg branches of certain IFMs; Internally managed AIFs; UCITS investment companies. |

| Recommended to Consider | Open-ended specialized investment funds (SIFs) not governed by Part II of the 2007 Law; Open-ended UCIs subject to Part II of the 2010 Law managed by a registered AIFM. |

2. Main Categories of Liquidity Management Tools (LMTs) under Circular CSSF 26/910: ESMA Guidelines on Liquidity Management Tools (LMTs) of UCITS and open-ended AIFs

The guidelines group the tools into three main sections based on how they function.

A. Quantitative-Based LMTs

These tools focus on controlling the amount or timing of money moving in and out of the fund.

- Suspensions: Temporarily stopping all subscriptions (buying) and redemptions (selling).

- Redemption Gates: Limiting the amount of money that can be taken out of the fund during a specific period.

- Extension of Notice Periods: Requiring investors to give more time before they can withdraw their money.

- Redemptions in Kind (RiK): Giving investors actual assets (like stocks or bonds) instead of cash when they leave the fund.

B. Anti-Dilution Tools (ADTs)

These tools focus on the cost of trading. They ensure that the investors who are buying or selling pay for the costs of those trades, rather than the investors who stay in the fund.

- Redemption Fees: A charge paid by the investor when they sell their shares.

- Swing Pricing: Adjusting the fund’s price (Net Asset Value) based on the amount of trading activity.

- Dual Pricing: Using different prices for buying and selling shares.

- Anti-Dilution Levy (ADL): A specific charge added to a trade to cover the costs of buying or selling the underlying investments.

C. Side Pockets

This involves separating illiquid or hard-to-value assets from the rest of the fund’s healthy assets.

3. General Principles for Selection and Use under Circular CSSF 26/910: ESMA Guidelines on Liquidity Management Tools (LMTs) of UCITS and open-ended AIFs

Fund managers must follow specific principles when choosing which tools to use.

Selection and Suitability

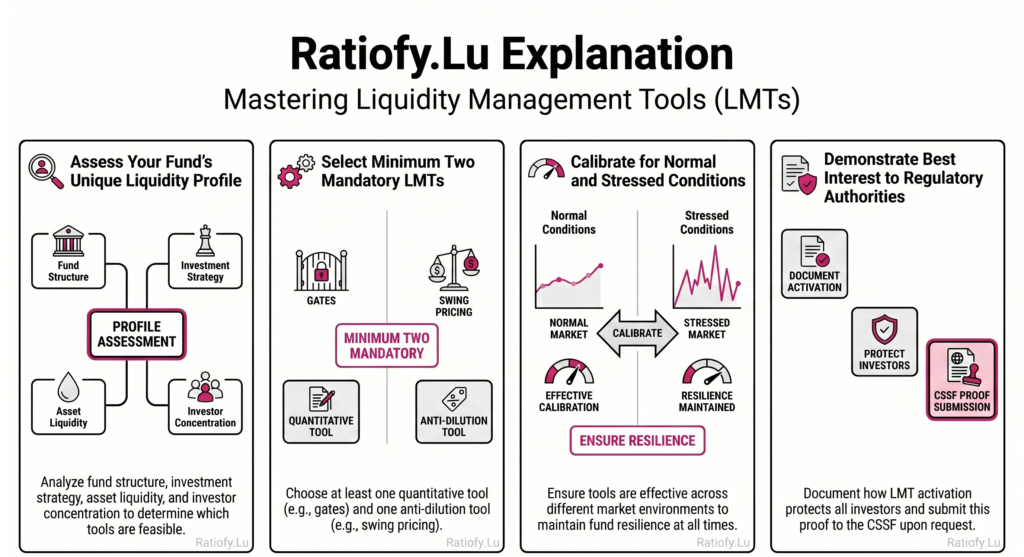

Managers are required to select at least two LMTs from the approved lists. It is recommended that they choose at least one quantitative tool and one anti-dilution tool. When selecting, they must consider:

- The fund’s legal structure and investment strategy.

- The liquidity profile (how easily the fund’s assets can be turned into cash).

- The results of “stress tests” (simulations of bad market conditions).

- The type of investors in the fund and the fund’s distribution policy.

- Any operational barriers or complexities.

Activation and Calibration

- Normal vs. Stressed Markets: Managers should have tools ready for both everyday market conditions and times of high financial stress.

- Investor Interest: Any decision to activate a tool must be in the best interest of all investors. Managers must be able to prove this to the CSSF if asked.

- Confidentiality: Managers must ensure that certain investors do not get “inside info” about when a tool might be activated, as this could give them an unfair advantage.

- Fair Valuation: Using anti-dilution tools does not change the manager’s duty to value all fund assets fairly at all times.

4. Key Deadlines under Circular CSSF 26/910: ESMA Guidelines on Liquidity Management Tools (LMTs) of UCITS and open-ended AIFs

The implementation of these guidelines follows a specific schedule:

| Date | Event |

| March 12, 2026 | Publication of the ESMA Guidelines. |

| April 15, 2026 | CSSF issues Circular 26/910. |

| April 16, 2026 | The Guidelines officially apply to new funds and authorities. |

| April 16, 2027 | The Guidelines apply to funds that existed before April 16, 2026. |

5. Reporting and Compliance under Circular CSSF 26/910: ESMA Guidelines on Liquidity Management Tools (LMTs) of UCITS and open-ended AIFs

- Competent Authorities: Agencies like the CSSF must notify ESMA within two months of the guidelines’ publication if they comply or intend to comply.

- Fund Managers: While managers are not required to report their compliance directly to ESMA, they must be ready to demonstrate to the CSSF that their selection and use of tools are fair, effective, and reasonable.

- Exceptional Circumstances: If unforeseen events make it impossible for a fund to meet its payment obligations, these tools become vital for maintaining order and fairness.

This news related to Circular CSSF 26/910 can be considered beneficial under CSSF-Circulars, EU Regulations, Explanation, IFMs (AIFMs, ManCos) News, Investment Firms News, Undertakings for collective investment (UCIs).

At https://Ratiofy.Lu/, we defend your hard-earned money with our free daily news platform and expert-vetted templates. Need more help? Request access to our hands-on expert Advisory, Training and Coaching Services (very limited availability) related to CSSF Circulars and EU Regulations.

The pre-filled example templates for many CSSF Circulars should be available at https://ratiofy.lu/templates/ from the summer of 2026.

5 Big Changes Coming to Investment Funds under Circular CSSF 26/910: ESMA Guidelines on Liquidity Management Tools (LMTs) of UCITS and open-ended AIFs

Why Your Investment Fund Needs a “Safety Valve”?

Imagine an investment fund as a shared pool of capital where every investor has contributed a portion of the total assets. In a stable market, the flow of investors entering and exiting is manageable, and the fund’s liquidity remains balanced. However, during periods of heightened market volatility, a significant problem can arise: what happens if a disproportionate number of investors attempt to withdraw their capital at the exact same time? This intense redemption pressure can force a fund to sell assets hastily, potentially at fire-sale prices, which can destabilize the fund for those who remain.

To address this risk, European and Luxembourg regulators—specifically the European Securities and Markets Authority (ESMA) and the Commission de Surveillance du Secteur Financier (CSSF)—are introducing a standardized framework of “Liquidity Management Tools” (LMTs). These rules act as a regulatory safety valve, ensuring that fund managers have the necessary mechanisms to maintain order during market stress. Ultimately, these changes are designed to ensure that all investors are treated equitably, whether they are redeeming their shares or staying invested for the long term.

1. The Manager Takes Full Responsibility under Circular CSSF 26/910: ESMA Guidelines on Liquidity Management Tools (LMTs) of UCITS and open-ended AIFs

Under the new CSSF Circular 26/910 and accompanying ESMA Guidelines, the role of the Investment Fund Manager (IFM) is being significantly fortified. Managers are no longer passive adherents to a regulatory checklist; they are the “captains” of the vehicle, expected to exercise professional judgment to protect the fund’s integrity.

Regulators have clarified that managers cannot wait for external intervention during a crisis. They must proactively select, calibrate, and activate the tools best suited to their fund’s specific investment strategy and investor base. Crucially, this is not a “set and forget” requirement. Managers have an ongoing duty to regularly review and recalibrate these tools to ensure they remain effective as market conditions evolve.

“The primary responsibility for liquidity risk management, as well as for the selection, calibration, activation and deactivation of LMTs, remains with the fund managers.”

2. The “At Least Two” Rule for Extra Safety under Circular CSSF 26/910: ESMA Guidelines on Liquidity Management Tools (LMTs) of UCITS and open-ended AIFs

To ensure that funds are not caught ill-prepared, the new regulations mandate that managers select at least two LMTs from a prescribed list. However, from an industry analyst’s perspective, the high-value insight lies in the “mix and match” recommendation provided by the CSSF.

The guidelines suggest that IFMs should consider selecting at least one quantitative-based LMT (such as redemption gates or notice periods) and at least one Anti-Dilution Tool (ADT). By maintaining this dual-layered defense, a fund is equipped to handle both “normal” market fluctuations and “stressed” periods of extreme volatility. This tiered approach ensures the manager has a proportional response ready for any level of redemption pressure.

3. Protecting the People Who Stay (Anti-Dilution) under Circular CSSF 26/910: ESMA Guidelines on Liquidity Management Tools (LMTs) of UCITS and open-ended AIFs

One of the most critical concepts in fund management is the protection of the Net Asset Value (NAV). When investors exit a fund, the costs of selling assets and the associated transaction fees can “dilute” the value of the fund for the remaining participants. Historically, this created a “first-mover advantage,” where investors rushed to exit first to avoid being saddled with these costs.

To eliminate this incentive for panic, the new rules emphasize the use of a full suite of Anti-Dilution Tools (ADTs). These include:

- Swing Pricing: Adjusting the NAV to reflect transaction costs.

- Redemption Fees: Direct charges paid by the exiting investor to the fund.

- Dual Pricing: Offering different prices for buying and selling shares.

- Anti-Dilution Levy (ADL): A specific fee calculated to cover the cost of liquidating assets.

By ensuring that “leavers” pay the true costs of their own exit, the “stayers” are protected from value erosion, maintaining the fund’s stability for the long term.

4. Using “Side Pockets” to Separate Trouble under Circular CSSF 26/910: ESMA Guidelines on Liquidity Management Tools (LMTs) of UCITS and open-ended AIFs

In rare instances, a fund may hold assets—such as bonds from a defaulted issuer or securities in a frozen market—that become suddenly illiquid or impossible to value or sell. In the past, these “toxic” assets could paralyze an entire fund, forcing a total suspension of redemptions for all investors.

The new guidelines promote the use of “side pockets” as a sophisticated structural solution. This allows a manager to move problematic assets into a separate “folder,” isolated from the healthy portion of the portfolio. By separating the trouble, the main fund can continue to calculate its NAV and process redemptions normally, ensuring that a single distressed asset doesn’t lock up your entire savings.

5. Preventing Information Leaks under Circular CSSF 26/910: ESMA Guidelines on Liquidity Management Tools (LMTs) of UCITS and open-ended AIFs

A vital, yet often overlooked, component of the new guidelines involves the prevention of “information leaks.” The regulator mandates that managers must prevent any specific group of investors from gaining insight into the “probability” that a safety tool, such as a redemption gate, might be activated.

This is a matter of market fairness. If a large institutional investor were to learn that a gate was 90% likely to close the following day, they might redeem their entire position immediately to avoid being trapped. Such an information imbalance directly harms retail investors who lack that access. By maintaining strict confidentiality until a formal announcement is made to the entire market, the CSSF ensures a level playing field for everyone.

The Important Dates under Circular CSSF 26/910: ESMA Guidelines on Liquidity Management Tools (LMTs) of UCITS and open-ended AIFs

The implementation of these safety standards follows a clear regulatory roadmap:

- April 16, 2026: The new rules apply to all newly launched investment funds.

- April 16, 2027: Existing funds are granted a twelve-month grace period to update their prospectuses, recalibrate their tools, and ensure full compliance.

Conclusion: A Safer Future for Your Savings

These regulatory shifts represent a foundational strengthening of the European investment landscape. By empowering managers to act as active stewards, requiring diversified safety nets, and ruthlessly focusing on the protection of the NAV, the CSSF and ESMA are building a more resilient market. As an investor, your role is to stay informed. Now that you understand the mechanics behind how managers are being directed to safeguard your capital, will you look more closely at the “safety tools” and “liquidity management” sections in your fund’s next annual report?