Luxembourg Financial Regulatory News:

CSSF Circulars:

The Circular CSSF 26/911 and the accompanying ESMA Final Report outline the updated 2025 guidelines for conducting stress test scenarios within the Money Market Fund (MMF) sector. These regulatory documents require fund managers to simulate severe financial shocks, including geopolitical instability, heightened asset volatility, and significant liquidity disruptions, to ensure fund resilience. The updated framework specifically recalibrates risk parameters for interest rates and credit spreads based on the systemic risk assessments provided by European financial authorities. Luxembourg-based managers must integrate these new standards into their administrative practices and utilize the revised benchmarks for their mandatory regulatory reporting starting in June 2026. Ultimately, these annual updates aim to maintain supervisory convergence and financial stability across the European Union by reflecting the most current market developments.

Summary

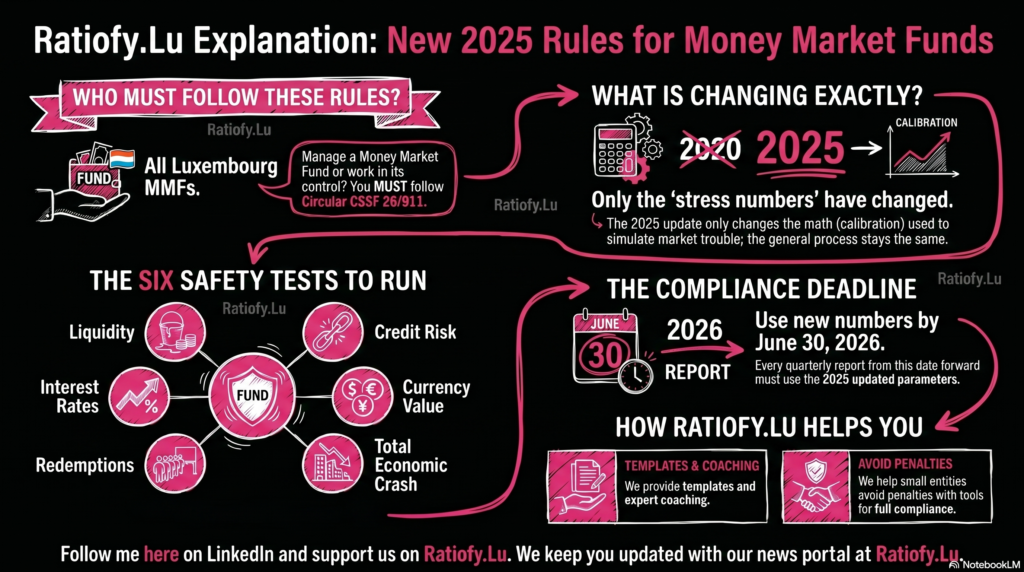

The Commission de Surveillance du Secteur Financier (CSSF) has issued Circular CSSF 26/911, which integrates the 2025 update of the European Securities and Markets Authority (ESMA) Guidelines on stress test scenarios for Money Market Funds (MMFs). Under Article 28 of the MMF Regulation (EU) 2017/1131, these guidelines are updated annually to reflect current market developments and systemic risks.

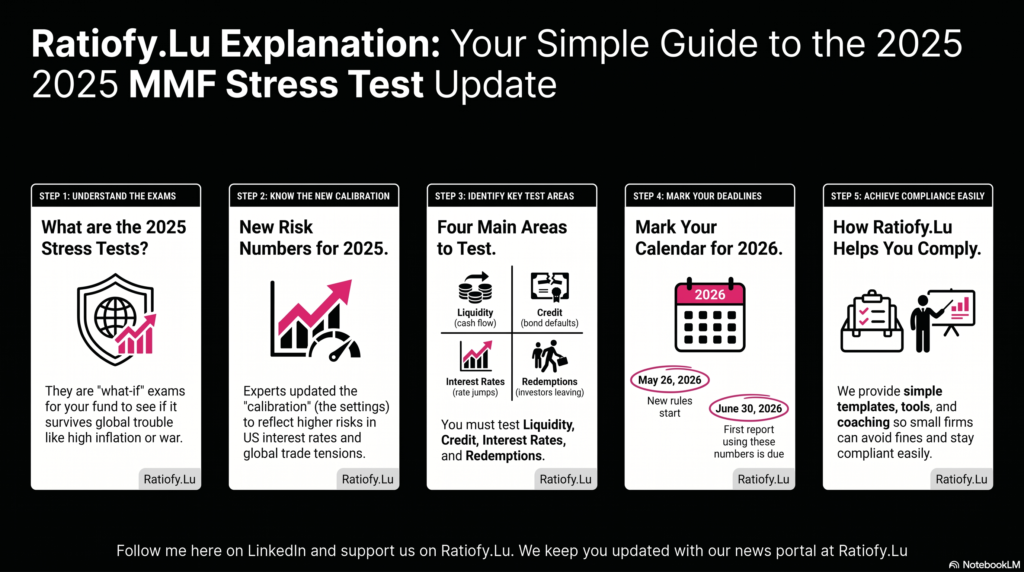

The 2025 calibration is characterized by a severe adverse scenario driven by elevated geopolitical uncertainty, trade disruptions, and resurgent inflationary pressures. While most stress testing frameworks remain consistent with previous years, the 2025 update introduces specific recalibrations for risk parameters, including shifts in EUR and USD swap rates, government bond spreads, and bid-ask spreads.

Main points under Circular CSSF 26/911: ESMA Guidelines on stress test scenarios under Article 28 of the Money Market Fund Regulation – Update 2025 (ESMA50-481369926-30585):

- Effective Date: The new guidelines enter into force on 26 May 2026.

- Reporting: All MMFs under CSSF supervision must apply these parameters for reporting periods starting from 30 June 2026.

- Primary Changes: Shocks to USD swap rates and government bond spreads have increased, while EUR swap rate shocks and bid-ask spread shocks are slightly reduced compared to the 2024 exercise.

- Risk Environment: Scenarios are calibrated to reflect “tail risks” stemming from global trade tensions and multiple worldwide conflicts identified as of November 2025.

Regulatory Framework and Scope under Circular CSSF 26/911: ESMA Guidelines on stress test scenarios under Article 28 of the Money Market Fund Regulation – Update 2025 (ESMA50-481369926-30585)

The document outlines the integration of ESMA Guidelines (Ref. ESMA50-481369926-30585) into the Luxembourg regulatory framework. This update replaces the 2024 version introduced by Circular CSSF 25/877.

Applicability

- Entities: All MMFs under CSSF supervision and Luxembourg-based managers of MMFs.

- Scope of Testing: Stress tests must assess the impact of various factors on the MMF’s portfolio, net asset value (NAV), liquidity buckets, and the manager’s ability to meet redemption requests.

- Legal Basis: Article 28 of the MMF Regulation requires “sound stress testing processes” to identify potential unfavorable economic conditions.

The 2025 Macroeconomic Stress Scenario under Circular CSSF 26/911: ESMA Guidelines on stress test scenarios under Article 28 of the Money Market Fund Regulation – Update 2025 (ESMA50-481369926-30585)

The calibration for 2025, developed in collaboration with the European Systemic Risk Board (ESRB) and the European Central Bank (ECB), is based on a narrative of high geopolitical instability and market volatility.

Systemic Risk Drivers under Circular CSSF 26/911: ESMA Guidelines on stress test scenarios under Article 28 of the Money Market Fund Regulation – Update 2025 (ESMA50-481369926-30585)

- Geopolitical Conflict: Global trade tensions and multiple conflicts are expected to amplify trade disruptions.

- Inflationary Pressure: Supply chain disruptions and rising commodity prices are projected to trigger resurgent inflation, causing a spike in risk-free rates.

- Financial Tightening: The combination of tighter financing conditions and sluggish economic growth is expected to drive asset price volatility.

- Debt Vulnerabilities: High government debt and weakened corporate debt-servicing capabilities—exacerbated by increased defense spending—are central to the 2025 risk assessment.

Market Impact Expectations under Circular CSSF 26/911: ESMA Guidelines on stress test scenarios under Article 28 of the Money Market Fund Regulation – Update 2025 (ESMA50-481369926-30585)

- Market Activity: An abrupt slowdown in market activity is anticipated, resulting in a sharp reduction in instrument liquidity.

- Asset Revaluation: Volatile conditions are expected to lead to an abrupt revaluation of financial assets and real estate prices.

- Sovereign Premia: Upward shifts in sovereign risk premia will vary across countries based on individual macroeconomic and fiscal positions.

Technical Recalibrations of Reference Parameters under Circular CSSF 26/911: ESMA Guidelines on stress test scenarios under Article 28 of the Money Market Fund Regulation – Update 2025 (ESMA50-481369926-30585)

The 2025 Guidelines update Section 5 (Calibration) while leaving the core methodology of Sections 4.1 through 4.7 largely unchanged.

Comparative Summary of Parameter Changes

| Parameter | 2025 Change (Relative to 2024) | Rationale |

| EUR Swap Rates | Slightly Lower | Reflects high uncertainty/volatility driving down demand. |

| USD Swap Rates | Higher | Linked to an uncertain outlook for the US economy. |

| Govt. Bond Spreads | Slightly Higher | Reflects elevated levels of government debt and fiscal positions. |

| Bid-Ask Spreads | Smaller | Calibration is less severe, but the probability of this scenario is increasing. |

| Redemption Levels | Unchanged | Parameters remain calibrated to the 2020 COVID-19 crisis levels. |

Liquidity and Asset Valuation Formulae

For additional common reference stress test scenarios, managers must apply specific discount and price impact factors to calculate an adjusted price ():

Managers are required to simulate the sale of a vertical slice of the fund portfolio (selling the same percentage of each asset) to meet redemption requests in these scenarios.

Core Stress Test Categories under Circular CSSF 26/911: ESMA Guidelines on stress test scenarios under Article 28 of the Money Market Fund Regulation – Update 2025 (ESMA50-481369926-30585)

MMFs are required to conduct tests across several hypothetical scenarios. While the guidelines provide minimum requirements, managers must tailor these to their fund’s specific risk profile.

- Liquidity Risk: Assessing the gap between bid and ask prices, trading volumes, and the number of active counterparties in secondary markets.

- Credit Risk: Simulating downgrades or defaults of major portfolio positions, including parallel shifts in credit spreads.

- Interest and Exchange Rates: Testing parallel and non-parallel shifts in the interest rate curve and movements in base currency versus other currencies.

- Redemption Stress: Calibrating scenarios based on the type of investor (institutional vs. retail) and liability concentration. This includes testing the “opt-out” of the most important investors.

- Spread Widening: Examining the narrowing or widening of spreads among indexes to which portfolio securities are tied.

- Macro-Systemic Shocks: Using adverse scenarios related to GDP or replicating historical global shocks.

Implementation Timeline under Circular CSSF 26/911: ESMA Guidelines on stress test scenarios under Article 28 of the Money Market Fund Regulation – Update 2025 (ESMA50-481369926-30585)

The transition from the 2024 to the 2025 guidelines follows a strict regulatory window:

- 13 January 2026: ESMA publishes the Final Report on 2025 Guidelines.

- 26 March 2026: Publication of French and German translations on the ESMA website.

- 19 May 2026: CSSF issues Circular 26/911.

- 26 May 2026: Entry into force; Circular CSSF 25/877 (2024 Guidelines) is repealed.

- 30 June 2026: First mandatory reporting date using the updated 2025 parameters.

Managers are instructed to continue using the 2024 parameters for all quarterly reports submitted prior to the 30 June 2026 reporting date.

This news related to Circular CSSF 26/911: ESMA Guidelines on stress test scenarios under Article 28 of the Money Market Fund Regulation – Update 2025 (ESMA50-481369926-30585) can be considered beneficial under CSSF-Circulars, Explanation, IFMs (AIFMs, ManCos) News, Must Read, Undertakings for collective investment (UCIs).

At https://Ratiofy.Lu/, we defend your hard-earned money with our free daily news platform and expert-vetted templates. Need more help? Request access to our hands-on expert Advisory, Training and Coaching Services (very limited availability) related to CSSF Circulars and EU Regulations.

The pre-filled example templates for many CSSF Circulars should be available at https://ratiofy.lu/templates/ from the summer of 2026.

Stress Testing the Chaos: 5 Key points from the 2025 Global Market Scenarios under Circular CSSF 26/911

In the world of financial regulation, there is a recurring irony: the more we use the word “unprecedented,” the more it becomes our baseline. For anyone monitoring the pulse of the European money market fund (MMF) space, the transition from the 2024 to the 2025 ESMA Guidelines marks the moment where “tail risks”—those once-in-a-generation catastrophes—have officially been codified as the standard operating environment.

The Commission de Surveillance du Secteur Financier (CSSF) recently signaled this shift by issuing Circular CSSF 26/911, integrating the 2025 ESMA Guidelines into the Luxembourg regulatory framework. As an analyst, what I find most telling is that while the bedrock of the framework (Sections 4.1 to 4.7) remains untouched, the regulators have surgically updated Section 5—the Calibration section. This is where the real “meat” of the 2025 scenarios lives, adjusting the dials of the financial system to account for a world that feels increasingly volatile.

These aren’t just bureaucratic exercises; they are high-stakes simulations calibrated to ensure that when the “unthinkable” happens, our funds don’t just survive—they remain liquid. Here are the five key takeaways from the 2025 guidelines.

1. Geopolitics is No Longer a “Side Risk” – It’s the Driver under Circular CSSF 26/911: ESMA Guidelines on stress test scenarios under Article 28 of the Money Market Fund Regulation – Update 2025 (ESMA50-481369926-30585)

In previous years, geopolitics was often treated as an exogenous shock—a “what if” scenario. In the 2025 guidelines, it is the primary engine of the entire risk model. The ESMA calibration, developed with the ESRB and ECB, moves away from isolated events toward a systemic chain reaction.

The logic flow is specific and unforgiving: heightened geopolitical tensions lead to trade disruptions, which trigger spikes in commodity prices. This, in turn, causes significant supply-chain disruptions, fueling inflationary pressures that force risk-free interest rates to spike.

The regulators are blunt about the severity of this outlook:

“The shocks have been calibrated to be severe, consistent with the materialisation of tail risks amid elevated geopolitical uncertainty stemming from global trade tensions and multiple conflicts worldwide.”

This isn’t just a “bad day” at the office; it’s a simulated environment of “sluggish economic growth” and “tightening financing conditions” designed to see who stays standing when the music stops.

2. The Great Divergence: USD vs. EUR Swap Rates under Circular CSSF 26/911: ESMA Guidelines on stress test scenarios under Article 28 of the Money Market Fund Regulation – Update 2025 (ESMA50-481369926-30585)

One of the most fascinating technical updates in the 2025 reference parameters is the divergent treatment of the world’s two major reserve currencies. While the shocks applied to USD swap rates have increased, the shocks for EUR swap rates are actually slightly lower than in the 2024 exercise.

At first glance, a lower EUR shock might seem like a reprieve, but the analyst in me looks at the “why.” The source context clarifies that these lower EUR shocks reflect “high uncertainty and volatility driving down demand.” It is a sobering reminder that a “smaller” shock can actually be a symptom of a more stagnant or fearful market. Conversely, the increased USD shocks are a reaction to a “more uncertain economic outlook for the US economy” and a shift in the calibration sample. For fund managers, this divergence means your “global” strategy needs to be far more nuanced than a one-size-fits-all interest rate hedge.

3. The Liquidity Paradox: Smaller Shocks, Higher Probability under Circular CSSF 26/911: ESMA Guidelines on stress test scenarios under Article 28 of the Money Market Fund Regulation – Update 2025 (ESMA50-481369926-30585)

The 2025 guidelines offer a strange paradox regarding market liquidity. Shocks to bid-ask spreads are technically smaller than in previous years. However, ESMA explicitly warns that while the calibration is less severe, its “probability is increasing.”

To address this, the guidelines lean heavily on the “price impact parameter.” This is a crucial technical nuance: the cost of liquidation is not static. Under the formula (), the impact is cumulative. The more a fund sells to meet redemptions, the higher the price impact factor becomes, eating away at the fund’s value in a downward spiral.

Furthermore, the guidelines demand the use of “slicing” rather than a “waterfall” approach. In a simulation, a manager might be tempted to “window dress” their results by assuming they only sell their most liquid, high-quality assets (the waterfall). Regulators now require a “vertical slice” simulation—selling a proportional percentage of every asset in the portfolio. It is a regulatory guardrail designed to prevent managers from hiding the true illiquidity of their back-books.

4. Sovereign Debt: A Country-by-Country Minefield under Circular CSSF 26/911: ESMA Guidelines on stress test scenarios under Article 28 of the Money Market Fund Regulation – Update 2025 (ESMA50-481369926-30585)

The risk associated with government bonds is trending upward, with shocks to spreads being “slightly higher” than in 2024. The 2025 scenario paints a grim picture of a “sovereign minefield” where debt servicing capabilities are weakened by:

- Elevated levels of government debt.

- Increased defense spending.

- Persistent high interest rates.

The takeaway here is that sovereign risk is no longer monolithic. Because macroeconomic and fiscal positions vary so wildly between nations, sovereign risk premia will shift differently across borders. Managers can no longer assume that a “flight to quality” into any government bond will provide the same haven; they must now stress test for a world where some sovereigns are significantly more fragile than others.

5. The COVID-19 Legacy: Redemption Levels as the Gold Standard under Circular CSSF 26/911: ESMA Guidelines on stress test scenarios under Article 28 of the Money Market Fund Regulation – Update 2025 (ESMA50-481369926-30585)

Perhaps the most telling part of the 2025 guidelines is what remains unchanged. The parameters for hypothetical redemption levels have not been touched since they were recalibrated during the 2020 COVID-19 crisis.

The regulatory consensus is that the 2020 event represented a true “maximum level of severity.” By keeping these parameters static, the ESMA and CSSF are acknowledging that the liquidity crunch seen at the start of the pandemic remains the definitive “worst-case” benchmark. It is a rare moment of regulatory stability, providing a fixed point of reference in an otherwise shifting sea of parameters.

Final Thought: Beyond the Minimum Requirements under Circular CSSF 26/911: ESMA Guidelines on stress test scenarios under Article 28 of the Money Market Fund Regulation – Update 2025 (ESMA50-481369926-30585)

As we look toward the implementation of Circular CSSF 26/911, which officially enters into force on May 26, 2026, the industry must prepare for the first mandatory reporting date of June 30, 2026.

It is vital for market participants to remember that these ESMA parameters are merely “minimum requirements.” The CSSF expects managers to go further—tailoring their stress tests to the specificities of their funds and layering in additional factors like repo rates where relevant. In an era where “tail risks” are the new normal, fund managers must ask themselves a difficult question: Is your internal stress testing merely a box-ticking exercise for the CSSF, or is it a true diagnostic tool capable of protecting your investors from the next geopolitical shift?