Luxembourg Financial Regulatory News:

Circular CSSF 25/901 modernises and consolidates the regulatory framework for Luxembourg’s specialised investment funds (SIFs), investment companies in risk capital (SICARs), and Part II UCIs. By repealing and replacing several older circulars, it establishes a single, simplified text that adapts existing core principles to practical experience. The circular provides comprehensive guidance on key operational and structural rules, including the definition of eligible assets, specific risk-spreading principles and investment limits, and the defining characteristics of risk capital for SICARs. Furthermore, it establishes strict transparency requirements, dictating how funds must disclose their investment policies, use of borrowing and portfolio management techniques, and redemption terms within their sales documents to ensure investors can make informed decisions.

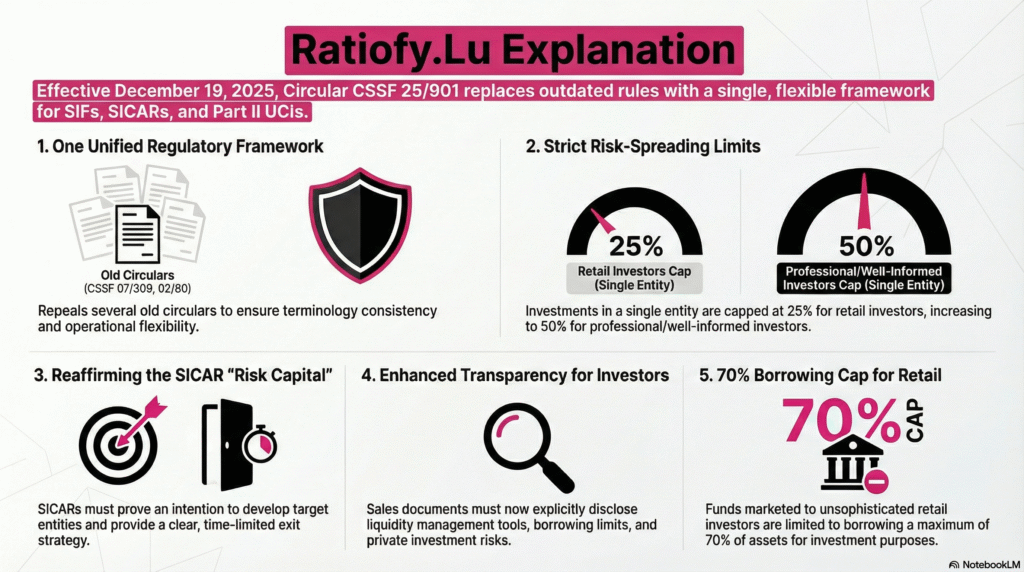

1. Introduction: The End of Regulatory Fragmentation under Circular CSSF 25/901 Relating to Specialised Investment Funds, Investment Companies in Risk Capital and UCIs

For decades, fund managers in Luxembourg have navigated a “regulatory maze,” stitching together compliance frameworks from a patchwork of legacy texts. Navigating the requirements of Circular IML 91/75 alongside Circular CSSF 02/80 often felt like trying to solve a puzzle where the pieces were designed in different eras.

The arrival of Circular CSSF 25/901 marks a major milestone for the world’s leading cross-border fund hub. By prioritizing “modernisation, clarification and simplification,” the Commission de Surveillance du Secteur Financier (CSSF) has provided a roadmap that updates the rules for Specialised Investment Funds (SIFs), Investment Companies in Risk Capital (SICARs), and Part II UCIs. This post distills the most impactful changes within this new, unified framework and what they mean for the future of private markets.

2. The Great Consolidation: One Text to Rule Them All under Circular CSSF 25/901 Relating to Specialised Investment Funds, Investment Companies in Risk Capital and UCIs

The most immediate benefit of the new circular is the repeal of several legacy regulations. By consolidating Circulars CSSF 02/80, 07/309, 06/241, and chapters of IML 91/75, the CSSF has created a single, consistent point of reference.

This consolidation is more than a cleanup; it is a strategic “future-proofing” of the Luxembourg toolbox. It finally bridges the gap between legacy standards—some dating back to the pre-AIFMD era—and the modern regulatory landscape.

The Scope and the “Grandfather” Clause: The circular applies to all SIFs, SICARs, and Part II UCIs. However, it explicitly excludes funds already governed by specific European labels, such as ELTIFs, MMFs, and EuVECA/EuSEF funds. Crucially for existing managers, the circular contains a “grandfathering” provision: it does not call into question the rules of closed-ended funds or compartments authorized before the circular enters into force on December 19, 2025.

“This circular is part of a broader effort towards modernisation, clarification and simplification.”

Reflection: For the strategist, this represents a shift toward operational maturity. By harmonizing terminology, the CSSF is reducing the “legal friction” that has historically bogged down fund launches and compliance monitoring.

3. The “Unsophisticated” Guardrails: Capping the Risk under Circular CSSF 25/901 Relating to Specialised Investment Funds, Investment Companies in Risk Capital and UCIs

As we witness the “retailization” of private assets, the CSSF has introduced clear guardrails for “unsophisticated retail investors”—defined as retail investors under AIFMD who do not meet the legal criteria of “well-informed.”

The 25% Limit and the “Look-Through” Strategic Win: For funds marketed to this retail segment, the CSSF generally limits investment to 25% of assets or commitments in a single entity or vehicle. However, the circular provides a vital exception for fund-of-funds: this 25% limit does not apply if the target vehicle itself ensures a comparable or stricter level of risk-spreading.

In contrast, funds reserved for “Well-Informed” or “Professional” investors enjoy higher thresholds, typically 50% (and up to 70% for infrastructure investments).

Reflection: These limits provide the structural safety net required to democratize private markets. The “look-through” provision is particularly significant for fund-of-funds managers, allowing them to build diversified retail-facing products without being hampered by arbitrary caps, provided the underlying assets are themselves diversified.

4. SICARs Are Not Holding Companies: The “Intention to Develop” Rule under Circular CSSF 25/901 Relating to Specialised Investment Funds, Investment Companies in Risk Capital and UCIs

One of the most critical clarifications concerns the nature of “risk capital” within SICARs. The CSSF is essentially “gatekeeping” the SICAR’s favorable status by demanding proof of active value creation. A SICAR is not a passive holding company; its investments must be characterized by an “intention to develop” the target entity through restructuring, modernization, or active management.

The Exit Strategy Mandate: The circular explicitly requires an exit strategy. Investments must be limited in time, with the objective of reselling for a profit. SICARs are now expected to describe these strategies and expected holding periods in their sales documents.

Reflection: By emphasizing “active intervention,” the CSSF is reinforcing the original spirit of the SICAR Law. This prevents the vehicle’s misuse as a passive tax-efficient wrapper and ensures it remains a tool for genuine economic development and entrepreneurial support.

5. Capping the Risk: The New Retail Leverage Reality under Circular CSSF 25/901 Relating to Specialised Investment Funds, Investment Companies in Risk Capital and UCIs

Borrowing powers have been clarified to prevent excessive systemic risk for the public. For SIFs or Part II UCIs marketed to unsophisticated retail investors, borrowing for investment purposes is now strictly capped at 70% of assets or commitments.

While professional and well-informed funds retain the flexibility to set their own limits, they must still disclose these maximums clearly in their sales documents.

Analysis: This 70% ceiling strikes a vital balance. It provides enough “dry powder” for managers to amplify returns while protecting retail participants from the catastrophic volatility that can accompany high-leverage private market strategies.

6. The “10-Year Commitment” and the 1+1+1 Rule under Circular CSSF 25/901 Relating to Specialised Investment Funds, Investment Companies in Risk Capital and UCIs

Transparency regarding liquidity mismatch is a major theme in the new text. For funds investing significantly in private assets with a life cycle or lock-up period exceeding ten years, a mandatory warning is now required.

The Prudent Person Advice: The warning must be specific: it must advise the average subscriber to invest only a portion of the sums they have allocated to long-term investments. This is a classic “Prudent Person” approach to investor protection.

The “1+1+1” Flexibility: To balance this transparency with performance, the circular introduces a new rule for private equity managers: funds can extend their life by one year, up to three times (1+1+1), if such extensions are necessary to allow investments to reach their full potential.

7. Flexibility Through “Duly Motivated Justification” under Circular CSSF 25/901 Relating to Specialised Investment Funds, Investment Companies in Risk Capital and UCIs

Despite the new limits, the CSSF maintains its “flexible yet firm” philosophy, allowing for derogations based on “duly motivated justifications.”

Ramp-up and Wind-down Benefits:

- Ramp-up: Funds focused on private investments have up to 4 years to build their portfolio, with a potential one-year extension.

- Wind-down: Crucially, the circular notes that for private investment funds, investment limits can cease to apply during the wind-down period.

Analysis: This operational flexibility acknowledges the reality of the private equity lifecycle. Allowing limits to fall away during liquidation prevents “fire sales” and ensures managers can focus on maximizing value for investors during the exit phase.

8. Conclusion: A Forward-Looking Framework under Circular CSSF 25/901 Relating to Specialised Investment Funds, Investment Companies in Risk Capital and UCIs

Effective December 19, 2025, Circular CSSF 25/901 is the foundation for the next generation of the Luxembourg fund industry. By replacing fragmented legacy rules with a unified, transparent, and modernized text, the CSSF has reinforced Luxembourg’s position as a premier global hub.

As regulatory barriers fall in favor of clear, unified standards, will we see an even faster migration of retail capital into the private markets? With the new “guardrails” and “look-through” provisions firmly in place, the framework is now ready for the era of democratization.

This news related to Circular CSSF 25/901 can be considered beneficial under CSSF-Circulars, Credit Institutions News, Explanation, IFMs (AIFMs, ManCos) News, Pension funds News, PFS/PSF News, and Undertakings for collective investment (UCIs).

The pre-filled example templates for many CSSF Circulars should be available at https://ratiofy.lu/templates/ from the summer of 2026.