Luxembourg Financial Regulatory News:

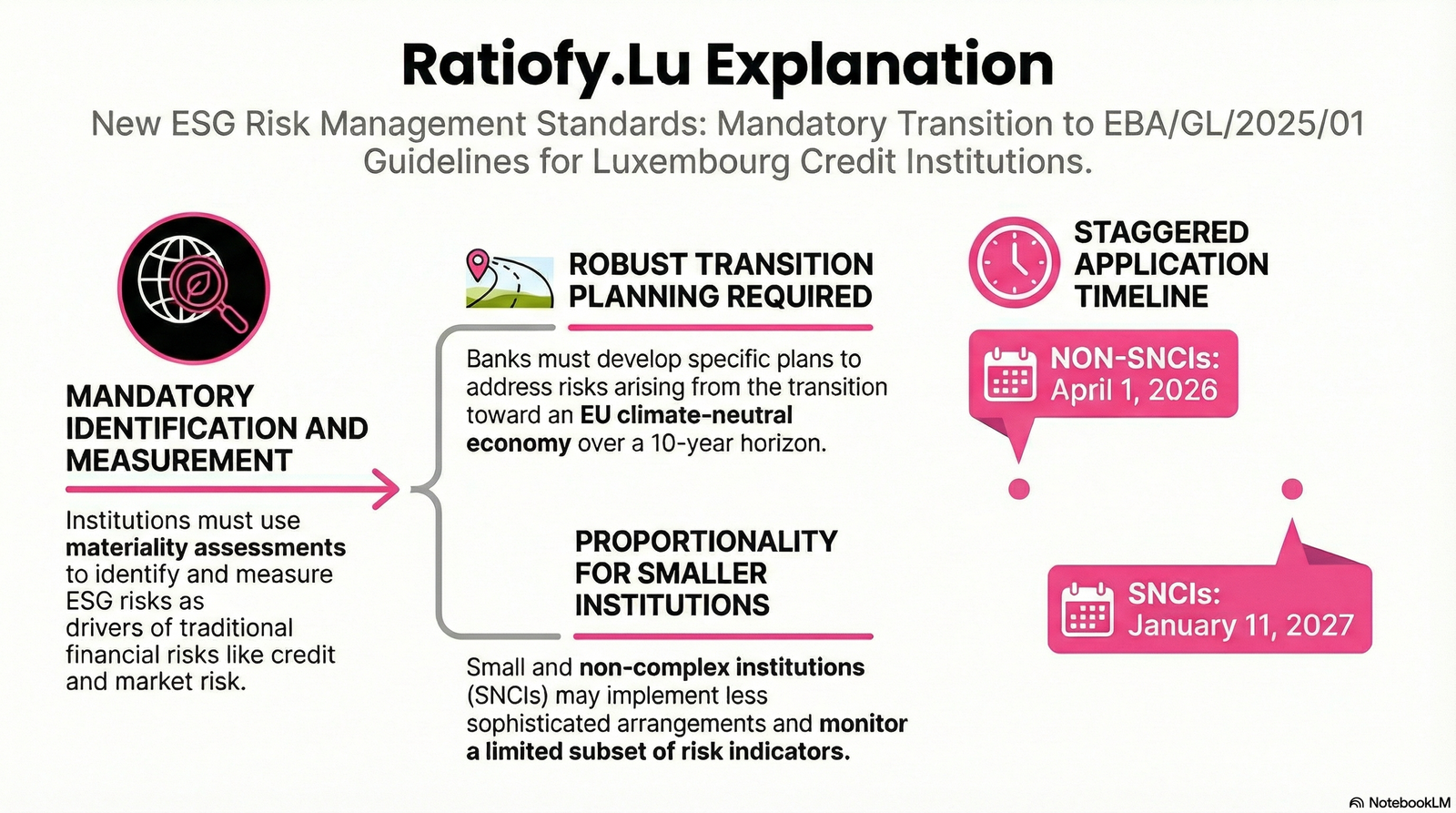

Circular CSSF 26/905 formally integrates the European Banking Authority’s Guidelines (EBA/GL/2025/01) on the management of environmental, social, and governance (ESG) risks into Luxembourg’s supervisory framework for Less Significant Institutions (LSIs). The circular requires these institutions to establish robust internal processes for the identification, measurement, management, and monitoring of ESG risks, which includes developing specific plans to address risks arising from the transition to an EU climate-neutral economy. To ensure a proportionate approach, Small and Non-Complex Institutions (SNCIs) and other non-large institutions are permitted to implement less complex risk management arrangements. The new regulatory requirements will apply from 1 April 2026 for non-SNCI Less Significant Institutions, while SNCIs are granted an extended implementation timeline until 11 January 2027, during which time the amended Circular CSSF 21/773 will continue to apply to them.

For a long time, the banking sector has operated within comfortable three-to-five-year medium-term cycles, a timeframe that fundamentally clashes with the multi-decadal, slow-burning reality of global climate change. That era of reconciliation by “green” buzzwords is over. As of January 2025, the European Banking Authority (EBA) has issued its final report on the management of Environmental, Social, and Governance (ESG) risks, effectively weaponizing ESG as a mandatory pillar of the prudential framework. This isn’t a voluntary reporting exercise to satisfy stakeholders; it is a total reconfiguration of the risk inventory designed to ensure the fundamental “safety and soundness” of financial institutions in a rapidly destabilizing climate.

Takeaway 1: The End of the ESG Silo (Risk as a “Driver”) under Circular CSSF 26/905, applying EBA Guidelines on ESG risks (EBA/GL/2025/01)

Regulators have officially dismantled the ESG silo. ESG factors are no longer a standalone category for niche sustainability departments; they are now classified as primary “drivers” that operate through specific transmission channels to infect traditional financial risks. A strategist understands that identifying the channel—such as how a localized flood leads to a credit default via collateral degradation—is now as vital as the risk category itself.

Underpinned by the concept of double materiality, institutions must assess both the “outside-in” financial materiality (how ESG factors hit the balance sheet) and the “inside-out” environmental and social materiality (how an institution’s impact on the world translates back into reputational and litigation risk).

The guidelines mandate that institutions assess these drivers across:

- Credit Risk: Directly embedding ESG into internal credit scoring and the valuation of collateral.

- Market Risk: Analyzing volatility in traded assets and shifts in market preferences.

- Operational Risk: Specifically focusing on the rising tide of ESG-related litigation.

- Liquidity Risk: Assessing sudden funding outflows or the illiquidity of “brown” assets.

- Business Model, Reputational, and Concentration Risk: Identifying excessive exposure to sectors vulnerable to transition shocks.

“Institutions should embed ESG risks within their regular risk management systems and processes ensuring consistency with their overall business and risk strategies.”

Takeaway 2: The “10-Year Minimum” Vision under Circular CSSF 26/905, applying EBA Guidelines on ESG risks (EBA/GL/2025/01)

In a radical departure from traditional banking horizons, the EBA now mandates a strategic vision of at least 10 years. This extension is designed to align bank risk management with the EU’s 2050 Net Zero milestones, forcing boards to look far beyond the next bonus cycle.

The analytical challenge is significant: how does one quantify “biodiversity loss” or “transition shocks” a decade out when historical data is non-existent? The EBA’s solution is the qualitative bridge. Where quantitative data fails, institutions must use qualitative perspectives to support strategic assessments. In this new regime, a “lack of granular data” is no longer an acceptable excuse for a lack of a long-term resilience plan.

Takeaway 3: Engagement Over Divestment (The Prudential Plan) under Circular CSSF 26/905, applying EBA Guidelines on ESG risks (EBA/GL/2025/01)

A critical distinction must be made between disclosure-led initiatives like the CSRD and the new CRD-based plans. While CSRD focuses on public transparency, CRD-based plans are for prudential risk management. They are not necessarily for public consumption; they are for the Supervisory Review and Evaluation Process (SREP), where regulators will scrutinize an institution’s survival strategy.

The EBA makes it clear that the goal is not a panicked exit from carbon-intensive sectors, which could destabilize the economy. Instead, it favors “engagement” as the primary risk management tool.

“The goal of CRD-based plans is not to force institutions to exit or divest from greenhouse gas-intensive sectors but rather to stimulate institutions to proactively reflect on technological, business and behavioural changes driven by the transition.”

Under these guidelines, the cessation of a relationship is a “last resort,” triggered only when a client’s trajectory is fundamentally incompatible with the bank’s long-term survival.

Takeaway 4: The “Proportionality” Buffer and Critical Timelines under Circular CSSF 26/905, applying EBA Guidelines on ESG risks (EBA/GL/2025/01)

While the regulator acknowledges that “size is not a sufficient criterion” for immunity to ESG risks—a small bank can still be sunk by a concentrated exposure to a flood zone—it does provide a tiered implementation schedule. Strategists must note the nuance between general EBA dates and local administrative applications.

| Feature | Large Institutions (Significant) | LSIs (Less Significant)* | SNCIs (Small & Non-Complex) |

| Application Date | 11 January 2026 | 1 April 2026 | 11 January 2027 |

| Materiality Assessment | Annual | Annual | Every two years |

| Data Sophistication | Granular client-level data | Granular client-level data | Estimates and proxies |

| Methodologies | Complex scenario-based modeling | Scenario-based modelling | Less complex arrangements |

*Note: Per Circular CSSF 26/905, the 1 April 2026 date applies to Luxembourg LSIs other than SNCIs.

Takeaway 5: Granular Data – Moving Beyond Proxies under Circular CSSF 26/905, applying EBA Guidelines on ESG risks (EBA/GL/2025/01)

The era of “estimates and proxies” is being phased out for larger players. Regulators now expect institutions to demand specific, client-level data from corporate counterparties to fuel their risk models.

Key data points now required include:

- Emissions Profile: Scope 1, 2, and 3 GHG emissions (absolute and intensity).

- Resource Dependency: Revenue tied to fossil fuels and, critically, water demand and consumption.

- Physical Vulnerability: Precise geographical location of production sites to assess solid mass-related hazards (landslides), water-related risks, and wind/temperature hazards.

- Real Estate Metrics: Energy efficiency levels (EPCs) tied to the borrower’s debt servicing capacity.

- Social/Governance Compliance: Adherence to UN Guiding Principles and the OECD Guidelines for Multinational Enterprises.

Conclusion: A Forward-Looking Summary under Circular CSSF 26/905, applying EBA Guidelines on ESG risks (EBA/GL/2025/01)

The shift toward “micro-prudential” transition planning represents the most significant change to bank supervision in a generation. These guidelines do not exist in a vacuum; they are the risk management teeth of a broader EU ecosystem including the CSRD and CSDDD. By requiring CRD-based plans, the EBA is ensuring that financial institutions are no longer just reporting on the weather, but are actively building ships capable of weathering the storm.

As the 2026 application date approaches, every board of directors must confront a singular strategic reality: “Is your institution viewing the transition to a climate-neutral economy as a regulatory hurdle to clear, or as the new blueprint for long-term financial resilience?”

This news related to Circular CSSF 26/905 can be considered beneficial under CSSF-Circulars, and Credit Institutions News.

The pre-filled example templates for many CSSF Circulars should be available at https://ratiofy.lu/templates/ from the summer of 2026.