Luxembourg Financial Regulatory News:

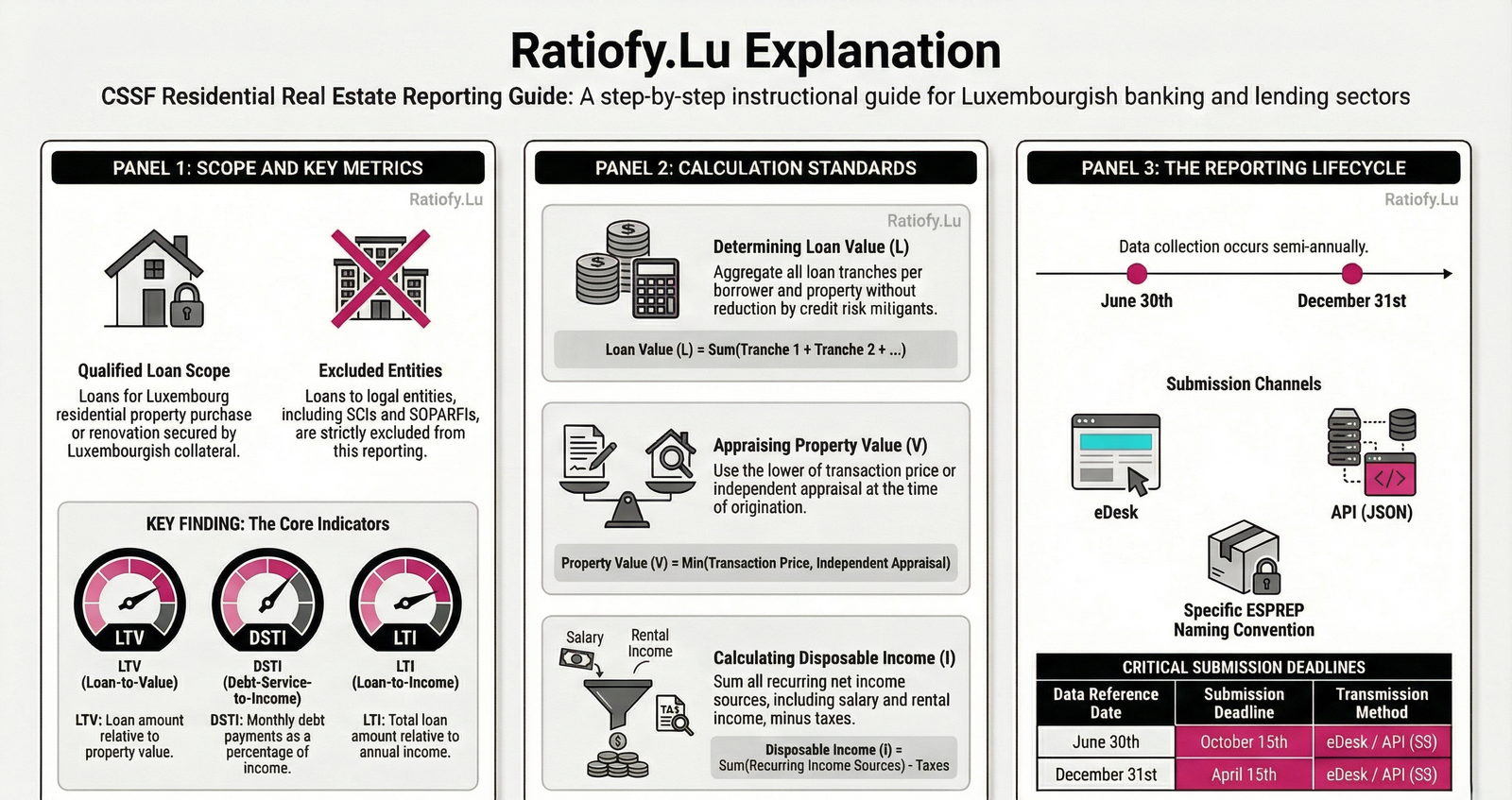

Circular CSSF 26/908 brings the regulatory update from the Commission de Surveillance du Secteur Financier (CSSF), which modifies existing guidelines for residential real estate lenders in Luxembourg. The document introduces updated semi-annual reporting requirements concerning specific borrower indicators, such as loan-to-value (LTV) and debt-to-income (DTI) ratios. These mandates apply strictly to natural persons seeking financing for local properties, intentionally excluding legal entities and commercial investments. Key revisions clarify how rental income is calculated and define the technical channels for data submission. Furthermore, the text provides precise methodologies for property valuation and the aggregation of debt across multiple loan tranches. Overall, these measures ensure that the financial supervisory authority maintains an accurate, current overview of the mortgage market’s risk profile.

Navigating the Luxembourgish property market often feels like deciphering a high-stakes puzzle. In a landscape defined by a structurally high Loan-to-Value (LTV) and Debt Service-to-Income (DSTI) environment, both borrowers and financial institutions operate under intense scrutiny. While the market’s dynamism is well-known, maintaining systemic stability requires a constant, granular recalibration of how risk is measured and reported.

Enter “Circular CSSF 26/908.” Though it may sound like another layer of dry bureaucracy, this document is a pivotal amendment to the foundational Circular CSSF 18/703. It signals a sophisticated evolution in the Grand Duchy’s regulatory oversight. This update isn’t merely a request for more data; it is a strategic refinement of the resolution of that data, ensuring that the risks underpinning the nation’s residential real estate (RRE) sector are understood with surgical, near-real-time precision.

By pulling back the curtain on these technical adjustments, we can see a regulator moving beyond the surface level of lending. From the way renovation costs are weighted to the digital pipes through which data now flows, these changes reflect a broader “FinTech-ification” of oversight. They signal a shift toward a more transparent, data-driven financial ecosystem that prioritizes market integrity over simple volume.

1. The “Natural Person” Boundary under Circular CSSF 26/908 (Amendment of Circular CSSF 18/703)

A primary pillar of Circular 26/908 is the strict delineation of its scope. The reporting requirements for residential indicators are intentionally restricted to natural persons. For a strategic analyst, this is a clear move to silo “household” risk from “commercial” risk, preventing the noise of corporate structures from skewing residential metrics.

Lenders must understand that loans granted to legal entities—even those used for investment purposes—are excluded from this specific RRE reporting. However, this debt does not vanish from the regulator’s view. Instead, credit provided to entities like Sociétés civiles immobilières (SCIs) or SOPARFIs is captured under Commercial Real Estate (CRE) reporting and the AnaCredit framework. This ensures that the CSSF maintains a “pure” data set for the residential market while still tracking broader leverage across the economy.

“Loans that are granted to a legal entity should not be included in the reporting. This implies that loans granted indirectly to natural persons for investment purposes through ‘Société civile immobilières’ or SOPARFIs are excluded from the reporting.”

2. The Rental Income Revolution (Variable I) under Circular CSSF 26/908 (Amendment of Circular CSSF 18/703)

The circular introduces a significant amendment to the calculation of borrower income, categorized as “Variable I.” This is a “disposable income” metric, strictly defined as the sum of all recurring income sources net of taxes, social security contributions, and health insurance premiums.

The “revolution” here lies in the formalization of rental income. Lenders are now mandated to include rental income using the best data available. Where precise figures are missing, banks must provide “best estimates” and a transparent description of their methodology. From a risk management perspective, the regulator also allows for—and expects—the application of “haircuts” to account for the inherent irregularity of investment income. This ensures that while the lending process becomes more inclusive of modern buy-to-let strategies, it remains grounded in conservative cash-flow reality.

3. Tightening the LTV on “Fixer-Uppers” under Circular CSSF 26/908 (Amendment of Circular CSSF 18/703)

When a borrower acquires a property requiring renovation, the regulator is now more prescriptive about how those improvements impact the “Value at Origination” (Variable V). Circular 26/908 limits the extent to which renovation costs can augment a property’s value to a range of 0% to 80% of the official estimates (devis).

This rule is a strategic safeguard against the creation of “synthetic equity.” By capping the fraction of renovation costs that count toward the property’s value, the regulator effectively tightens the Loan-to-Value (LTV) cap for fixer-uppers. It prevents lenders and borrowers from over-leveraging based on speculative future valuations that may never materialize in a market downturn.

“The lender should define internal policies to guide decisions on the fraction of renovation costs that will augment the value and follow them systematically.”

4. The Firewall: Article 208(3) and Appraiser Independence under Circular CSSF 26/908 (Amendment of Circular CSSF 18/703)

To preserve the structural integrity of the market, the CSSF has reinforced the “Independence” requirements for property valuation. Explicitly referencing Article 208(3) of the CRR Regulation, the circular mandates a strict “firewall” between the commercial units driving loan volume and the units responsible for appraisal.

This independence is not just for human appraisers; it applies equally to the development and application of valuation models or RRE indices. If a current value is calculated in-house, it must be performed by a unit such as Risk Management, entirely separate from commercial agents. This prevents the inherent conflict of interest where a financial incentive to close a deal might otherwise influence the valuation of the underlying collateral.

5. Regulation Goes High-Tech (JSON and S3) under Circular CSSF 26/908 (Amendment of Circular CSSF 18/703)

The most visible sign of the “FinTech-ification” of Luxembourgish regulation is the shift in transmission standards. The CSSF is moving away from legacy channels like E-file and SOFiE toward more automated, structured data exchange.

Starting in 2024, lenders have the option to submit data via the eDesk Portal or an API solution. The latter utilizes a structured JSON format transmitted via the S3 (Simple Storage Service) protocol. This move toward API-based reporting allows for faster data processing and more agile oversight, moving the regulator closer to the technological standards of the very FinTechs they supervise.

Deep Dive: The LTV vs. LTV_FP Distinction under Circular CSSF 26/908 (Amendment of Circular CSSF 18/703)

For the expert analyst, one of the most nuanced changes is the separate tracking of LTV (Loan-to-Value) and LTV_FP (Loan-to-Value of the Financed Property). While “V” generally represents the total collateral (which may include multiple properties), “V_FP” focuses specifically on the value of the property being purchased. By tracking these as separate statistics, the CSSF can identify where borrowers are using existing equity in other properties to juice their leverage on new purchases—a vital metric for spotting localized bubbles.

A More Transparent Horizon under Circular CSSF 26/908 (Amendment of Circular CSSF 18/703)

The implementation of Circular CSSF 26/908, with its semi-annual reporting cadence every April and October, marks a new chapter in Luxembourg’s financial maturity. While these rules necessitate a higher degree of technical and operational readiness from lenders, they ultimately build a more resilient foundation for the economy. By refining how income is netted, how renovations are valued, and how data is digitally piped to the regulator, the Grand Duchy is ensuring its real estate market remains as stable as it is dynamic.

In an era of high-tech oversight, will more data finally lead to a more stable and accessible housing market for everyone?

This news related to Circular CSSF 26/908 can be considered beneficial under CSSF-Circulars and Credit Institutions News. The pre-filled example templates for many CSSF Circulars should be available at https://ratiofy.lu/templates/ from the summer of 2026.