Luxembourg Financial Regulatory News:

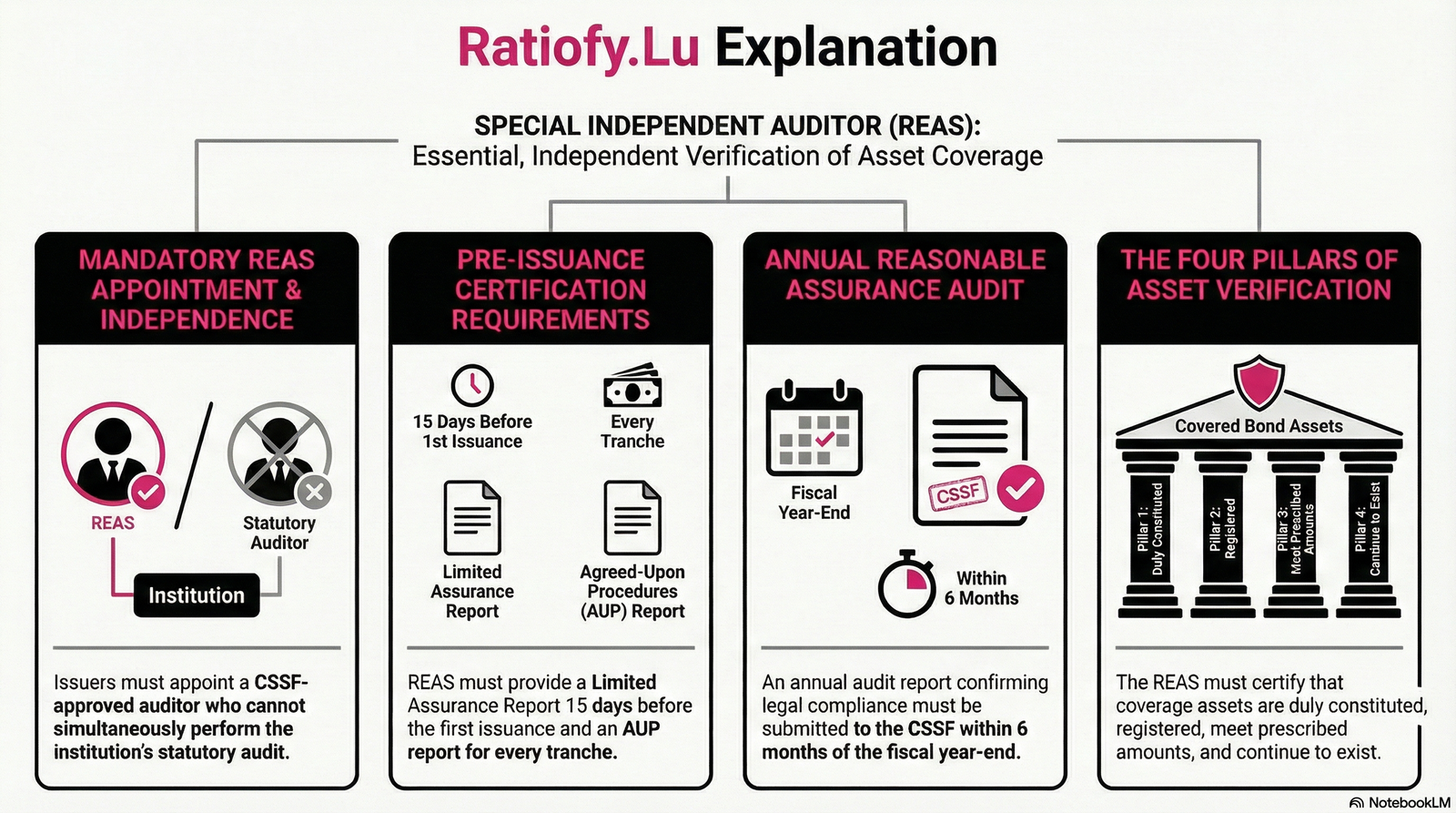

Circular CSSF 26/907 defines the specific supervisory and auditing requirements for credit institutions issuing covered bonds (lettres de gage) and outlines the strict duties of their special approved statutory auditors (REAS). The circular mandates that the REAS – who must possess the necessary expertise and cannot simultaneously act as the institution’s standard statutory auditor for financial accounts – is responsible for verifying the integrity of the cover pool both before and after any issuance. Prior to issuance, the REAS must produce a limited assurance report for the overall emission program and an agreed-upon procedures report for each specific tranche, ensuring that the cover assets are legally compliant, properly valued, and correctly inscribed in the pledge register. Furthermore, on an annual basis, the circular requires the REAS to submit a report providing reasonable assurance that the cover assets continuously meet all statutory requirements, specifically confirming that they remain duly constituted, properly segregated, correctly valued, and sufficient to cover the prescribed required amounts.

Introduction: The High Stakes of Trust under Circular CSSF 27/907 on Requirements Applicable to Special Réviseur d’Entreprises Agréé (approved statutory auditor) for credit institutions

In the upper echelons of European finance, the Luxembourg lettres de gage (covered bonds) have long been the gold standard for security. For institutional investors, these instruments represent a bedrock of stability, underpinned by high-quality assets and a rigorous legal framework. However, maintaining this level of trust in a shifting regulatory environment requires more than just historical prestige; it requires a structural upgrade.

Enter Circular CSSF 26/907. This directive from the Commission de Surveillance du Secteur Financier (CSSF) provides the technical manual for a new era of oversight, specifically defining the role of the réviseur d’entreprises agréé spécial (REAS)—the “special approved statutory auditor.” This isn’t just a routine update; it is a fundamental pivot toward a high-assurance framework where the auditor is no longer a passive reviewer of historical data.

Beyond the technical jargon lies a new operational reality for Luxembourgish banks: one where the auditor is no longer a post-mortem reviewer, but a real-time co-pilot in the issuance process. Below, we reveal the most impactful takeaways from this regulatory shift and what they mean for the future of the market.

1. The “No Double-Dipping” Rule: Strict Auditor Independence under Circular CSSF 27/907 on Requirements Applicable to Special Réviseur d’Entreprises Agréé (approved statutory auditor) for credit institutions

The CSSF is effectively personally vetting the individuals standing at the gates. Under Article 17 of the Law of 8 December 2021 (the “Law”), every credit institution issuing lettres de gage must appoint a REAS, but the Circular takes this a step further. Issuers must now communicate the names of specific principal audit partners to the CSSF for formal approval (Section 1.iii).

This is about more than firm-level compliance; it’s about individual accountability. To prevent any “double-dipping” or dilution of oversight, the Circular enforces an absolute “wall” between the bank’s general health and the covered bond’s security. The team auditing the bank’s corporate balance sheet is strictly forbidden from acting as the REAS for its covered bond programs.

“A statutory auditor or the partners of the same audit firm cannot simultaneously exercise the functions of REAS and the statutory auditor who performs the legal audit of the accounts.” (Circular Section 1.iv)

2. Granular Oversight: The Tranche-by-Tranche Requirement under Circular CSSF 27/907 on Requirements Applicable to Special Réviseur d’Entreprises Agréé (approved statutory auditor) for credit institutions

The new framework introduces a “lockstep” administrative burden that differentiates between the overarching program and the tactical issuance of debt. This is where the operational headache begins for issuers:

The Strategic Pre-requisite: At least 15 days before the very first issuance, the REAS must deliver a Limited Assurance report (ISAE 3000). This is a mandatory gate; without this report confirming the program’s compliance with legal coverage and registration requirements, the program cannot go live.

The Tactical Grind: For every single tranche (or “tap”) of the market, the REAS must provide a fresh Agreed-Upon Procedures report (ISRS 4400).

From a regulatory perspective, this means that every issuance is a unique event requiring specific, recurring auditor verification. There is no such thing as a “blanket approval” under Circular 26/907; the REAS must be engaged for every step, confirming that the assets backing that specific tranche meet the Law’s stringent criteria before the bonds can be issued.

3. The Auditor’s Veto: Real-Time Control Over the Pledge Register under Circular CSSF 27/907 on Requirements Applicable to Special Réviseur d’Entreprises Agréé (approved statutory auditor) for credit institutions

Perhaps the most significant shift in power is the REAS’s role as the guardian of the pledge register (registre des gages). In accordance with Article 15 and Article 17 of the Law, the “existence” of assets is not a one-time check but a real-time constraint.

Once an asset is inscribed in the register, it is legally “locked.” An issuer cannot simply swap or remove an asset to manage liquidity or balance sheet needs without the explicit, written consent of the REAS. This “Auditor’s Veto” ensures that assets are only released if the remaining pool satisfies not just the basic legal coverage, but the strict regulatory ratios—including those found in Articles 6, 8, and 9 of the Law.

“An asset included in the pledge register can only be removed with the written agreement of the REAS, it being understood that the REAS is required to consent to the removal… provided that the remaining coverage assets… are sufficient to cover the legal coverage requirements.” (Circular Section 4.iv.a)

4. Green Assets, Hard Math: The 180-Day Liquidity Mandate under Circular CSSF 27/907 on Requirements Applicable to Special Réviseur d’Entreprises Agréé (approved statutory auditor) for credit institutions

As Luxembourg cements its position in the green bond market, the CSSF is replacing “projections” with “hard math.” This is particularly evident in the valuation of renewable energy assets.

Under Article 17, paragraph 2, alinéa 4 of the Law, renewable energy equipment must undergo a mandatory annual re-evaluation. The REAS must ensure these values are grounded in current market data and adapted valuation assumptions, rather than stale appraisal cycles. Furthermore, the auditor is now responsible for verifying the “Hard Math” of liquidity. Per Section 4.iii.b, the REAS must audit the adequacy of the issuer’s process for determining cash flows to guarantee the liquidity of the cover pool for a rolling 180-day window.

This moves the auditor into the realm of cash-flow forecasting, ensuring that the “green” label is backed by both physical asset reality and robust 180-day liquidity buffers.

Conclusion: A Future of “Assurance-First” Banking under Circular CSSF 27/907 on Requirements Applicable to Special Réviseur d’Entreprises Agréé (approved statutory auditor) for credit institutions

Circular CSSF 26/907 signals a definitive departure from the “compliance-check” models of the past. By mandating personal partner vetting, tranche-level reporting, and real-time control over the pledge register, Luxembourg is positioning its lettres de gage framework as the de facto “Gold Standard” for the broader EU Covered Bond Directive.

As these stringent standards take hold, we must ask: Is the administrative cost of this extreme transparency the necessary price for ultimate market stability? In an era of global economic volatility, Luxembourg’s “assurance-first” model suggests that for those who value absolute security, the price is well worth paying.

This news related to Circular CSSF 26/907 can be considered beneficial under CSSF-Circulars and Credit Institutions News.

The pre-filled example templates for many CSSF Circulars should be available at https://ratiofy.lu/templates/ from the summer of 2026.