Luxembourg Financial Regulatory News:

Circular CSSF 25/899 formally integrates the European Banking Authority’s Guidelines (EBA/GL/2025/03) concerning Acquisition, Development, and Construction (ADC) exposures to residential property into Luxembourg’s regulatory framework. Applicable with immediate effect to Less Significant Institutions and Luxembourg-incorporated CRR investment firms, the circular aims to promote European supervisory convergence. The core focus of the adopted guidelines is to specify the credit risk-mitigating conditions that allow institutions to assign a reduced risk weight of 100%, instead of the standard 150%, to residential ADC exposures. Furthermore, the circular outlines specific tailored frameworks and considerations for applying these risk weights to loans granted to public housing and not-for-profit entities.

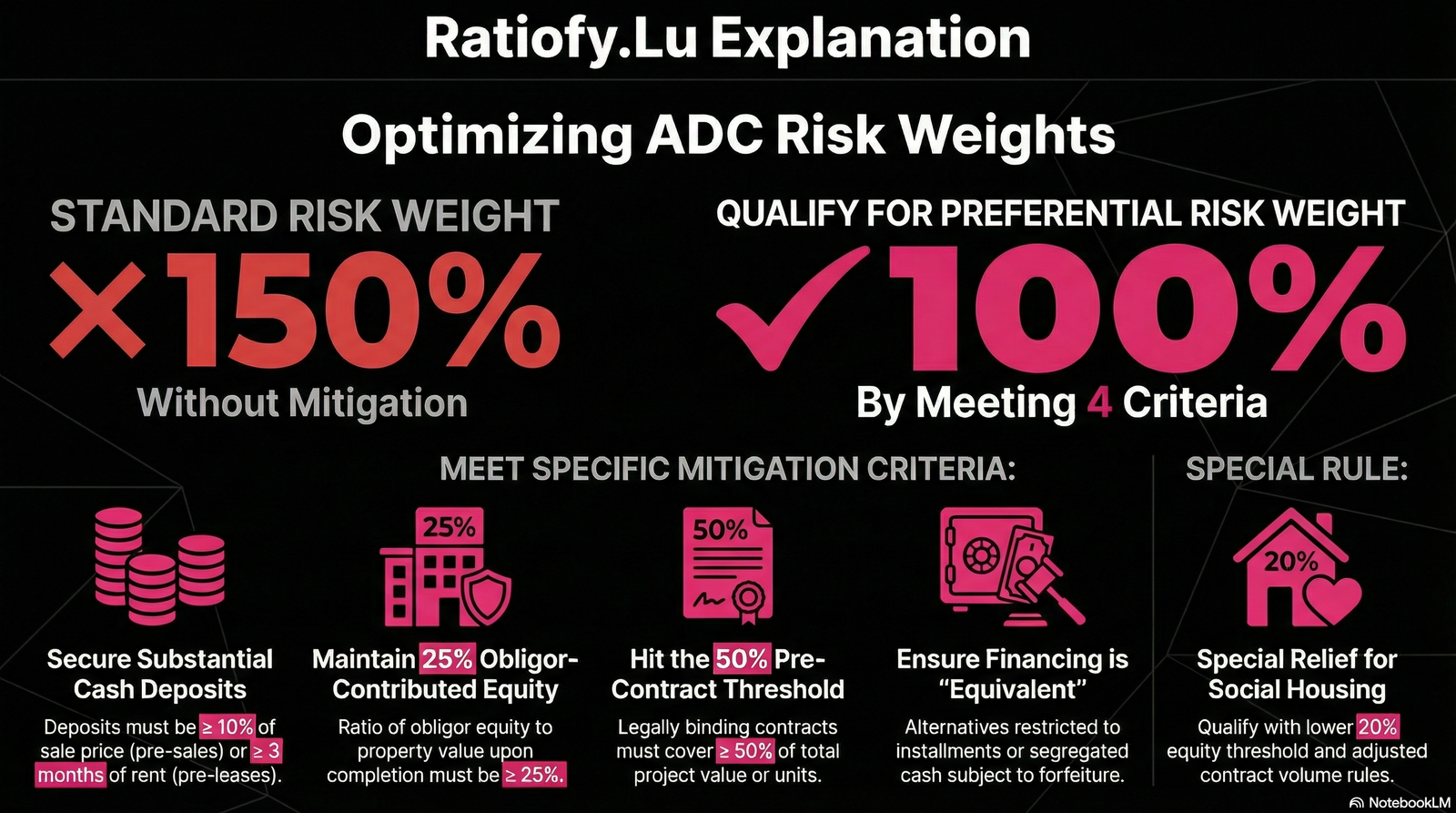

The High Stakes of ADC Financing under Circular CSSF 25/899 on Acquisition, Development, and Construction (ADC) exposures to residential property following EBA/GL/2025/03

Exposures related to Acquisition, Development, and Construction (ADC) carry a heavy burden under the Basel III framework. Traditionally, Regulation (EU) 575/2013 (CRR) assigns these exposures a 150% risk weight, effectively imposing a 50% capital surcharge compared to standard corporate lending. This “penalty” reflects the volatility of real estate development but exerts significant pressure on a bank’s balance sheet, often constricting the flow of credit to vital residential projects.

The European Banking Authority (EBA) has introduced a regulatory map to escape this high-capital environment via the EBA/GL/2025/03 guidelines. These rules specify the rigorous credit risk-mitigating conditions required to pivot from a 150% weight to a preferential 100% weight. By mastering these criteria, institutions can optimize their Risk-Weighted Assets (RWAs) and achieve superior capital efficiency in a competitive lending market.

This framework is about more than mere compliance; it is a catalyst for supervisory convergence and market stability across the EU. By standardizing what constitutes “preferential” risk, the EBA ensures that capital requirements accurately reflect the protection provided by high-quality contracts and developer equity. For the sophisticated lender, these guidelines represent a roadmap for balancing prudent risk management with the goal of RWA optimization.

The “Skin in the Game” Threshold: 10% Cash Deposits under Circular CSSF 25/899 on Acquisition, Development, and Construction (ADC) exposures to residential property following EBA/GL/2025/03

To qualify for the 100% risk weight, individual pre-sale and pre-lease contracts must be anchored by “substantial cash deposits.” For pre-sale agreements, the cash deposit must reach at least 10% of the sale price. In the case of pre-lease contracts, the threshold is set at 300% of the monthly rent—effectively a three-month commitment—to ensure the tenant is financially tethered to the project.

The regulatory intent behind these ratios is to create a “forfeiture-based incentive” that discourages buyer or tenant walk-aways. Beyond serving as a penalty, the EBA views these deposits as a necessary economic buffer to compensate the developer for market price deterioration. If a project is not converted and must be re-marketed at a lower price, these forfeited funds protect the project’s solvency and the bank’s recovery prospects.

The EBA defines the economic function of this requirement with technical precision:

“The cash deposit should be substantial enough to serve as an incentive for the purchaser or tenant to convert the pre-sale and pre-lease contracts into sale and lease contracts, thereby effectively reducing the risk of the default of the obligor.”

The 50% Marketability Test under Circular CSSF 25/899 on Acquisition, Development, and Construction (ADC) exposures to residential property following EBA/GL/2025/03

Individual contract quality is only half the battle; the EBA also mandates that these contracts cover a “significant portion” of the project. To hit the 50% marketability mark, developers must pass a calculation that varies based on the exit strategy. This test is designed to mitigate the risks inherent in an “absence or scarcity of marketability,” ensuring cash flows are sufficient for debt service upon completion.

The calculation methodologies are distinct: for sales, a Credit Facility Based ratio is used, dividing the sum of eligible sale prices by the total credit facility (including all drawn and undrawn amounts). For leases, the Simple Number ratio applies, where the number of eligible contracts is divided by the total number of units or potential contracts. This ensures that the project’s repayment source is structurally de-risked before the preferential risk weight is applied.

Navigating this requirement is particularly complex for mixed-use projects that include both sale and lease components. If a single credit facility finances the entire project, the developer faces a “double-hurdle”: they must hit the 50% threshold on both ratios simultaneously. Only if the lender grants separate facilities for the sales and lease portions can the 100% risk weight be applied at the individual facility level, provided repayment is strictly isolated to those respective cash flows.

The 25% Equity Shield under Circular CSSF 25/899 on Acquisition, Development, and Construction (ADC) exposures to residential property following EBA/GL/2025/03

The guidelines establish a rigorous, closed-loop eligibility framework for “appropriate” obligor-contributed equity. To secure the 100% risk weight, the developer must maintain a ratio of at least 25% equity relative to the property’s value upon completion. This “Equity at Risk” serves as a vital cushion, absorbing unexpected losses from adverse market movements before a final buyer is secured and the price is fixed.

The EBA permits only five specific forms of equity to count toward this 25% shield:

- Cash invested and segregated from the developer’s other assets.

- Subsidies and grants already invested to cover incurred project costs.

- Unencumbered readily marketable assets directly linked to the project and valued at market prices.

- Out-of-pocket expenses paid by the developer for development or construction.

- Land or improvements, which must be measured at their market value at the moment of contribution into the project.

This final requirement regarding land valuation is a critical safeguard against regulatory arbitrage. By pegging the value to the moment of contribution, the EBA ensures that the equity buffer represents real, tangible value rather than speculative gains. Furthermore, any “excess costs”—where total completion costs exceed the sustainable property value—must be deducted from the equity total to maintain a prudent buffer.

The Social Housing “Fast Track” under Circular CSSF 25/899 on Acquisition, Development, and Construction (ADC) exposures to residential property following EBA/GL/2025/03

Recognizing the unique structural demand for affordable housing, the EBA provides an optional, specialized framework for public housing and not-for-profit entities. In this sector, demand often structurally exceeds supply, reducing the marketability risk associated with traditional residential developments. This allows for a more flexible path to RWA optimization for developers regulated by social housing laws.

Social housing projects benefit from a 5% reduction in the equity threshold, requiring only 20% equity relative to the property’s value upon completion. Additionally, the guidelines allow for “committed” subsidies to be included in the equity calculation. This includes state-backed, unsecured junior loans with preferential rates, even if the funds have not yet been paid out to the obligor.

The “significant portion” requirement is also adjusted for social housing providers. A project can meet the marketability test if the number of applicants for units exceeds the available supply. Crucially, if project-specific applicant data is missing, the guidelines allow for the use of municipality-level data as a proxy. This ensures that social housing developments can access the 100% risk weight even where traditional pre-leasing is prohibited by local law.

Conclusion: A Harmonized Horizon under Circular CSSF 25/899 on Acquisition, Development, and Construction (ADC) exposures to residential property following EBA/GL/2025/03

The new EBA guidelines bring a high degree of technical clarity to ADC exposures, yet the “Escape Room” remains difficult to exit. While the rules offer a potential 10.6% reduction in risk-weighted assets, EBA data reveals that only 32% of current ADC exposures actually meet these strict eligibility conditions. This highlights a significant gap between current market practices and the new regulatory standard for “low-risk” development.

As institutions align their originating and monitoring standards with these rules, the competitive landscape of European real estate finance will shift. Lenders who proactively restructure their deals to meet these 10%, 25%, and 50% hurdles will gain a distinct capital advantage. Those who fail to adapt will remain trapped under the 150% capital surcharge, facing higher costs and diminished lending capacity.

A critical question remains: will the 10% cash deposit rule create a true level playing field across the Union, or will it prove too high for markets where national consumer protection laws traditionally cap deposits at lower levels? In such jurisdictions, the interplay between local law and the EBA’s prudential framework will determine which projects can truly qualify for preferential treatment.

This news related to Circular CSSF 25/899 can be considered beneficial under CSSF-Circulars, Credit Institutions News and Investment Firms News.

The pre-filled example templates for many CSSF Circulars should be available at https://ratiofy.lu/templates/ from the summer of 2026.